Start using your HELOC today. Here’s where to find HELOCs.

There are three main places you can look to find HELOCs.

Where to Find a HELOC

A HELOC is a lien against a property that is set up much like a credit card.

A financial institution will set it up for you with a:

Credit limit – the maximum you can borrow from the HELOC.

Term length – the amount of time the HELOC is available and the limit is locked in (usually around 10 years).

Methods to access the money – how you can borrow the money (bank wire, debit card, etc.).

1. Credit Unions

Firstly, look for a HELOC at a credit union. Credit unions will have the best HELOC rates and terms. We’ve found that to be universal state-to-state.

Shop around at local credit unions. Make sure the lender you’re working with likes real estate investors. Each lender has their own niche. One may prefer doing car loans, but another will prioritize HELOCs.

You’ll find the best deal from a credit union, but you should still shop around for the right one.

2. Local Banks

Secondly, look into a local bank.

Local banks usually like to work with real estate investors. They’ll have more products available as far as HELOCs for rental properties and HELOCs on multiple properties.

3. National lenders

Thirdly, look for a HELOC with national lenders.

Now that the refi-boom is settling down, national lenders and mortgage brokers are starting to offer HELOCs. Going through a national lender will open you up to more products, but the cost is almost guaranteed to be higher.

Consider all three of these options to find the best deal you can. For a HELOC, the “best” deal involves not just rate but LTV.

https://hardmoneymike.com/wp-content/uploads/2022/10/Where-to-find-helocs.png6991048Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-10-13 10:00:362022-09-13 16:36:27Where To Find HELOCs with the Best Terms

For your lender to feel comfortable, you need to know the ways to secure a gap loan.

When you hear the advice to “secure” your gap loan, what does that mean? How do you secure a gap loan? And why?

Ways to Secure a Gap Loan with Two Lenders

Securing your loan involves both your hard money lender and your gap lender.

Your friend or family member is giving you a fairly large chunk of money. They’ll want to know how you’ll secure it for them.

Securing your gap lender’s loan involves putting a lien on the property. Does your hard money lender allow this? Not all lenders will.

If Your Hard Money Lender Doesn’t Allow a Lien

If your hard money lender does not allow a lien on the property, you’ll have to secure the loan with a different property.

You could either put the lien on your own home, or you could use another rental or investment property.

If They Do Allow a Lien

If your hard money lender does allow a lien on the property to secure a gap loan, it’s best to do during closing with the mortgage and deed. This way title records it, and you have evidence for your gap funder that it’s recorded.

Many gap lenders – especially if they’re family or friends – won’t be educated enough about the real estate world to understand how to secure their money. As the investor, it’s your responsibility to keep your lenders’ money safe.

Securing the Gap Loan

No matter which property has the lien, you’ll have to take a few important steps to secure the gap loan.

You’ll need a note – a promissory note between you and your gap lender – and a lien, either a mortgage or a deed of trust. And you’ll have to record all this with the county.

To make sure the loan is concerned, be sure to check all these boxes. It’s important to do this thoroughly so your lender will:

https://hardmoneymike.com/wp-content/uploads/2022/10/secure-gap-loan.png6991048Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-10-12 10:00:022022-09-08 13:00:17Ways to Secure a Gap Loan & How to Do It

There are two types of HELOCs, primary vs secondary. Here’s what you need to know about them.

You can get a HELOC from two sources: the house you live in, and, potentially, some of your rental properties.

Primary Home – Primary vs Secondary HELOCs

HELOCs are calculated using LTVs and CLTVs (combined loan-to-values).

To calculate this, the bank looks at the loan balance for your first mortgage, plus what the HELOC will add to it. Then they divide that by the value of your home to get to the combined loan-to-value.

Most banks and credit unions will go up to 90% CLTV, but some do 100% on primary homes.

Using a HELOC unlocks all the equity you’ve established on your home as home values go up over the years.

Rental Properties – Primary vs Secondary HELOCs

Rental HELOCs are a little more limited. They have different LTV/CLTV requirements.

For rental properties, there are some banks, credit unions, and mortgage brokers that will allow HELOCs in second position that go up to a CLTV of 65% to 75%.

Different lenders will limit the amount of secondary HELOCs differently, but most will give you one or two properties.

When To Get a HELOC

Start using your HELOC now, before home prices go down.

If you have a lot of equity in your rental properties or home, you can tap into that now while the market’s still high. This limit will be locked in for 10 years, even as your home value will likely come down 5-10% in the next six to nine months.

If you wait to take out either primary or secondary HELOCs you’ll lose more of your available funds.

https://hardmoneymike.com/wp-content/uploads/2022/10/1-vs-2-helovs.png5941053Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-10-06 10:00:422022-09-13 16:28:45Primary vs Secondary HELOCs – A HELOC for Your Rental??

When your loan doesn’t cover 100% of your project, how do you calculate gap funding?

How much do you need for gap funding? It depends on each project.

Calculating Gap Funding Needed for a Project

The way to figure out the gaps in your project is simple:

(Cost of Property + Rehab Costs) – Hard Money Loan Amount = Gap Funding Amount Needed

If the property costs $200,000, but your lender gives $140,000, there’s a $60,000 gap you’ll need to cover. You can:

Pay the $60,000 out-of-pocket

Or

Bring in a gap lender, enabling you to buy the property with 100% financing. You would likely use part of this loan for the down payment and part for construction costs.

In case your loan is for LTV only and doesn’t take into account construction costs, here’s how you would calculate those costs for an undermarket home:

ARV – Actual Cost of Property = Maximum Construction Budget

It’s important for you to work these numbers and know your budget up-front. Keep in mind, it’s always better to err on the generous side with your numbers. You want to be sure you can get done on-time and within the budget allotted by your hard money and gap lenders.

How much you’ll spend on construction is important when you calculate gap funding.

https://hardmoneymike.com/wp-content/uploads/2022/10/calculate-gap-fund.png7061054Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-10-05 10:00:252022-09-08 12:58:39How to Calculate Gap Funding

It can come as a first, second, or sometimes even third mortgage. If you don’t owe anything on your house, you can put a HELOC in first position. With an existing mortgage, it’s put in second position.

It’s a Line of Credit

A HELOC is set up kind of like a credit card. The bank sets a limit they’ll lend and a term for how long.

A HELOC can pay for almost anything related to your projects. You can go to Home Depot and get materials, you can pay your contractors, you can make a down payment. It can take the form of a bank wire, a debit card, or whatever other option your bank gives you.

At the end of the month or the end of a project, you pay the HELOC off, and all the credit is freed up. You can use it again, pay it down, then use it again for as long as the term is active.

Typically, the bank will set a 10-year term. So for 10 years, you can use and re-use it up to the limit they set. If your property goes up in value during that time, it’s possible to get a refinance for a higher limit.

It’s a Faster, Easier, Cheaper Source of Money!

Any expenses you can put on a HELOC frees up your investment experience. When you borrow from other places (hard money lenders, banks, etc), there’s more paperwork and more cost.

HELOCs are easier, faster, and cheaper. A successful investor uses every leverage tool at their disposal, so it’s important to tap into this one.

https://hardmoneymike.com/wp-content/uploads/2022/09/what-is-a-heloc.png7091058Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-09-30 10:00:452022-09-13 16:20:51What Is a HELOC for Real Estate Investors?

Here are 5 ways to use hard money right as a real estate investor.

Real estate investing is all about making profit.

And sometimes, to make profit, you need to use hard money loans.

When is hard money your best option in real estate investing? Let’s look at 5 situations where you should use hard money to fuel your investments.

1. Using Hard Money for Speed

The number one way hard money makes you money in real estate investing is how fast they are.

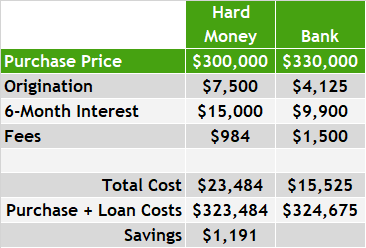

Look at a real example from one of our clients.

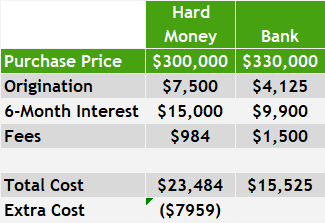

He was able to buy a property in Colorado at a $30,000 discount.

Five other people were bidding as high as $330,000 on the property.

But our client was able to close in less than a week, so the sellers accepted his bid of $300,000.

How Much Does a Hard Money Loan Cost?

People can get tripped up with the cost of hard money. Wouldn’t the price of the loan leave our client at a loss here? Let’s compare his hard money loan on this deal to his competitors with a bank loan.

For hard money, he spent $7,500 on origination. A bank loan would have cost $4,500.

Six months’ worth of interest on the hard money loan adds up to $15,000. The same time on a bank loan would accrue $9,900 of interest.

Appraisal underwriting, and processing fees were lower with hard money at $984 (vs $1500 with the bank.)

Overall, our client did pay a lot more for the loan itself using hard money. His hard money loan cost $23,484, and a bank loan would have cost $15,525. That’s an extra cost of $7,959 to use hard money.

Can You Save Money by Using Hard Money for Real Estate?

Despite seeming more expensive, hard money still gave this investor a discount. Why? Hard money enabled him to close fast, so he got a better deal on purchase price.

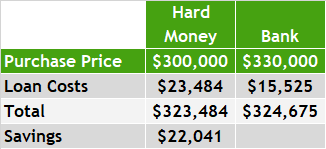

What was the total cost of hard money? The discounted price of the property ($300,000) plus the hard money loan costs equals $323,484.

What about the bank loan? The home price of $330,000 plus bank loan costs totals $345,525.

This is a savings of $22,041. Just for closing fast with hard money rather than using the cheaper but slower bank loan.

Using hard money for speed works even when the discount is smaller.

Let’s say our client had bid only 10,000 less than the other investors. He still would’ve saved $1,191 up front on the deal.

Hard Money Savings without a Purchase Price Discount

The option of buying real estate with bank loans is often cheaper. However, in many investment situations, using a bank loan is not a viable option.

If you have to wait 4 weeks to clear your bank loan, but only 4 days for a hard money loan… that becomes the difference between closing on the property or not.

Ultimately, even if using hard money doesn’t get you the lowest price, you still save money in the long run. If the speed of a hard money loan gets you a property, you will still come out on top.

Buying then selling a profitable fix-and-flip will always make more money than never buying and never selling.

2. Use Hard Money if You Have Low Credit

Institutional lenders, private equity, and banks have credit score minimums. If you don’t have a high enough score, you don’t get a loan.

Hard money lenders, on the other hand, are typically not credit-score-driven. Yes, they’ll probably look at your credit, but they won’t base your loan on it.

Real estate investors can have low credit scores for many reasons:

Usage – You put your flip rehab costs on credit cards

Thin Credit – You have few lines of credit, or young lines of credit

One-time Event – You had good credit, then life happened and your score temporarily dipped.

Hard money lenders understand that these issues are not always a reflection of your ability to pay back loans.

That’s why hard money lenders don’t worry about your credit score, just your credit.

Do you have a history of late payments? Are you defaulting? That will negatively affect you with a hard money lender.

If you are responsible with credit, but have a score banks won’t accept, a hard money lender will be a good option.

3. Using Hard Money Because It’s Flexible

Sometimes you need an outside-of-the-box lender.

Unique Properties – If you have a house or area that’s unique (maybe a dome house, an old manufacturer, etc.), hard money lenders will give you more options.

Rural Areas – Most local banks and large hard money lenders don’t lend outside of MSAs. Traditional lenders might not cover thirty miles outside of an urban area, but many small hard money lenders will.

Cross Liens – Hard money lenders have more flexibility putting a cross lien on another property. This is useful if you don’t have a lot of money to put down, but do have another property with a lot of equity.

Gap funding – Sometimes a mortgage doesn’t quite cover all the costs of your project. Hard money can fill in those gaps.

Lot splits – Splitting off a lot can be a headache with a traditional lender. A hard money lender is more flexible with the time it takes to get a survey and everything else prepared. This allows you to split off a lot, sell the house, and keep the lot.

Then rate-and-term refinance into a longer-term loan.

If you want to get into BRRRR transactions (rental properties), you have to find a hard money lender or private lender who will loan you 75-80% of the after-repair value of the property you want to buy.

There are many other reasons real estate investors use hard money. Here are a few:

Banks limit you to 2-3 loans. If you’ve maxed out those lenders, hard money can help.

Hard money can work as a bridge loan. It covers the down payment of your next property until your other bank-funded property sells.

You can keep a project off your credit. Hard money typically doesn’t show up on your credit report.

Investment beginners might need help with their first couple projects started before banks will lend to them.

Complete a started project. If you end up with a property mid-flip, many banks won’t lend for it. But a hard money lender can easily provide a gap loan to finish the rehab.

Hard money has the flexibility to let you come in with other funding sources. (If you want to put repair costs on a credit card, want to use an OPM lender, etc.).

How to Use Hard Money for Real Estate

Want to learn more about real estate funding? Wondering if a hard money loan might be right for your investment?

https://hardmoneymike.com/wp-content/uploads/2022/09/Oct-22-When-To-Use-HM-Blog-Thumbnail.png6001800Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-09-29 14:09:232022-09-29 14:09:235 Times You Should Use Hard Money for Your Real Estate Investments

Cash flow for BRRRR could take a big hit in 2022. Here are some alternatives to try.

We’re probably three to six months out from the really cheap homes getting on the market. How can you plan to finance BRRRRs as values go down but loan requirements go up?

BRRRRs are about getting into value-add properties with little to no money down. But as we’ve mentioned, getting into the properties will be the hard part with money tightening.

Will there be any good alternatives to BRRRR in 2022?

Subject Tos As Alternatives to BRRRR

Here’s another way to look at rental properties with a BRRRR spirit:

What if you could take over someone’s loan and house with no money down, no credit or other requirements, 100% financing, and a great rate?

That’s what subject tos are.

You’ll see more and more subject tos popping up soon. Maybe someone bought their home at 100% last year, but values have come down 10-15% so they can’t sell without losing money or putting more in. People don’t want to go through foreclosure, so in a situation like this, they’d be interested in a subject to.

You can take over the mortgage and put the home in your name. You can do it properly, through title, and create a rental property using someone else’s financing.

This is a great way to purchase rental properties as an alternative to BRRRR in 2022 if you don’t have leverage.

Owner Carries in 2022

An owner carry can happen when the seller owns a property free and clear. In this situation, the owner takes on the mortgage.

The seller would likely plan to invest the money they get when the house sells. But the stock market is up and down, and banks only offer 2% maximum interest rates in CDs and accounts.

For the owner, carrying the mortgage when they sell to you is a way to double or triple their interest rate, secured by an asset they already know.

For you, an owner carry is easier, cheaper money. You won’t find a 5% interest rate, with 100% financing and no credit check anywhere else.

Open-Minded Financing Alternatives During Inflation

There’s creative financing available in the real estate investment world.

Whether it’s subject tos, owner carries, or OPM relationships, it’s important to look always into your options for doing zero down investments. Especially now that loans are less likely to cover 100% financing, it’s important to stay open to alternatives to BRRRR in 2022.

Gap funding is a way to get $0 down BRRRR properties!

You should use gap funding for BRRRRs the same way you do fix-and-flips. The biggest differences happen at closing.

Similarities to Fix-and-Flips

Gap funding is used very similarly for both BRRRR and flips: for down payments, construction costs, or carry costs.

The bulk of the money not covered by a hard money lenders becomes the down payment. Most lenders require at least 10% for this cost.

Your primary loan does not always cover construction costs – rehab, repair, or anything necessary to bring the house up to the ARV and onto the market.

Also, some investors like to use gap funding for the carry costs of the project: the mortgage payment, the insurance, and all other monthly costs.

Gap funders can (and should) be used for all these phases of your BRRRR project.

Gap Funding Process During BRRRRs

Use BRRRR gap funding like fix-and-flip gap funding: for down payment, construction, or carry costs.

For BRRRR though, you need to close the gap funding loan on the same day as closing. You’ll also need to be sure you close the gap funding at the title company, with your lender. So you’ll need to know in advance that your hard money lender allows gap funding with a lien on the property.

Protecting Your BRRRR Refinance While Using Gap Funding

If you close your gap loan too late or incorrectly, your long-term lender can consider your refinance cash-out, not rate-and-term. This will lower the LTV on your refinance.

It’s important to get the money for your loan back in the refinance. In a good BRRRR transaction, you walk away with a house that’s cash-flowing and little to no money out of your pocket.

https://hardmoneymike.com/wp-content/uploads/2022/09/gap-fund-brrrr.png7051054Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-09-28 10:00:552022-09-08 12:18:16How to Use Gap Funding for BRRRR Projects

If you don’t use a HELOC in your real estate investment career, you’re missing out on these benefits.

The uses and benefits of a HELOC for a real estate investor are broad and huge. This line of credit is one of the best ways to tap into your existing money to create more money.

Let’s take a look at a few of the ways you can utilize your HELOC to benefit your real estate investments.

Benefits of a HELOC for Real Estate Investors

Down Payment

You can use a HELOC as a down payment on any loan – hard money or long-term. Anytime a lender requires a down payment, you can take the money off your home equity line of credit, and bring it to closing.

For down payments on rental properties, your lender will still require the money borrowed from your HELOC to be included in your debt ratio.

Construction Costs

For a flip or a BRRRR, you can use money from your HELOC to cover the costs of construction.

Money from a hard money lender or bank comes at a higher price. If you’d prefer to use your HELOC to cover construction costs, you can lower the amount borrowed from a lender.

A HELOC will be some of the cheapest money you can find out there – especially now with money tightening. Using it helps lower your overall costs.

Another benefit of a HELOC is the speed and flexibility. If you don’t have time to wait for your lender’s escrow process to pay your contractor, you can just pull the payment off your HELOC.

Carry Cost Benefits of a HELOC

Carry costs include monthly interest, HOA fees, mortgage payments, some materials and construction, and any other regular cost associated with owning the property.

These costs can turn into a burdensome expense on a flip. You can pull from your line of credit to cover carry costs, and when your flip sells, you can put it all back in.

The benefit of a HELOC here is that you don’t have to get lender approval or meet lender requirements before placing a bid on a property. You can pull from it, pay for the property (or at least the down payment), and refinance later if needed.

Buying Wholesale Properties

You can also buy properties from wholesalers or the regular marketplace when you otherwise couldn’t. You close with a HELOC, then go back and refinance with a hard money or bank loan.

With this strategy, you can close on a deal faster than anyone else. You don’t have to sift through the paperwork and red tape of a loan; just go to the bank and wire out the funds.

Bridge Loan Benefits of a HELOC

Some investors use their HELOC to bridge between properties.

They have one flip for sale, but they’re ready to buy their next one. They use a HELOC to cover the down payment, then pay it back when the other property sells.

You can create your own bridge loan by using a HELOC.

Lend to Other People

You can also use it to lend to other people in the real estate investment community at a profit.

You can borrow from a HELOC at a rate of 5-6%, and you could charge someone else up to 10-12%. (But of course, always be careful and protect yourself when lending to other people).

Overview of the Benefits of a HELOC

Using your HELOC allows you to use your money, without taking anything from your savings or 401k

You can tap into the equity that’s already at your disposal

It keeps projects going while typical loans are tightening up

You can get into properties quickly and refinance a few weeks later

You can avoid the higher rates of external lenders by borrowing from your HELOC

https://hardmoneymike.com/wp-content/uploads/2022/09/Benefits-of-a-heloc-2.png7111058Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-09-23 10:00:492022-09-13 13:08:47Benefits of a HELOC: Are You Missing Out?

Don’t walk into a loan without a plan – use gap funding for flips!

During a time when lenders are offering less money up-front for investment deals, you might need more money to fill in the gaps on your fix-and-flip projects.

Here are a few phases where you might need gap funding on your project.

Down Payments

Hard money lenders require at least 10% as a down payment. This is a very common use for gap funding.

If you use gap funding for your down payment, you’ll need to find out right away whether or not your hard money lender will accept a secured gap loan on the property.

Construction Costs

Another way to use gap funding for flips is for construction costs – rehab, repair, or anything necessary to bring the house up to the ARV and onto the market. These expenses can rack up fast, and they may not be completely covered by the main loan for the flip.

Carry Costs

Some investors will only use gap funding for the carry costs during their flip.

The lender will pay the mortgage payment, the insurance, or whatever other monthly costs are required during the project. Having a gap lender for carry costs can smooth out a fix-and-flip experience.

The Reach of Gap Funding for Flips

It’s possible to coordinate with your gap lenders to cover all three of these additional costs. This is a common way investors successfully finish fix-and-flips with zero money down.

You can use gap funding however you need, as long as both the hard money lender and the gap lender agree that the loan fits their criteria.

Not all hard money lenders allow you to secure your gap loan with a lien on the property you’re closing on. And not all gap lenders will loan to you unsecured.

https://hardmoneymike.com/wp-content/uploads/2022/09/gap-fund-flip.png7021054Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-09-22 10:00:172022-09-08 12:05:05How to Use Gap Funding for Your Flips

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.