Bridge Loan – What is it? Do I need one?

https://corporatefinanceinstitute.com/resources/knowledge/finance/what-is-bridge-loan/

https://corporatefinanceinstitute.com/resources/knowledge/finance/what-is-bridge-loan/

Quick to Buy, Quick to Refi, a new 2-step loan strategy, helps you maximize your loan amounts while limiting the amount of cash you put into a project. It also helps you rapidly finish your projects and buy again, and again, and again.

What does that all mean? It means you no longer need to worry about missing out on great deals and getting stuck in expensive hard money loans.

The Quick to Buy, Quick to Refi strategy all starts with properly setting up your short AND long-term loans.

Now, even though your short-term loan will come first (to quickly buy an under market property from a wholesaler), a key step is to FIRST get pre-qualified for the long-term loan. Why? To ensure you’re able to maximize both loan amounts. If you can qualify for a larger loan upfront, then it’s likely your short-term lender will match that amount.

It also means you’re already going through the process for securing a long-term loan as you begin renovating a property with a short-term loan. Think, “Two birds, one stone.” By the time you finish renovations, you’re ready to refinance into a long-term loan.

But, hold on. You also need to know about the types of refinances. There are two you need to know about: “rate and term” and “cash out”. And yes, it matters you know the differences.

Ready to find out what about those differences? Then check out the whole video here and start capturing free equity, boosting your cash flow, and investing in more properties.

Want more videos with more tips to maximize your cash flow? Then check out our new video page, or subscribe to our new YouTube channel! Be sure to also check out all of our invest tools.

BRRRR is great, but did you know there are 2 key pillars of BRRRR that most investors don’t know about? Whether you’re just starting out with real estate investing, or you’re an ol’ pro, you should consider taking advantage of these crucial steps to ensure you don’t miss out on cash boosting opportunities.

Take a look at this video and learn about the two key pillars of the BRRRR method.

If you invest in rental properties, then you need to:

These steps help you maximize your loan amount while limiting the cash you need to put into each deal. They also ensure you’re able to buy more deals and build your portfolio at a faster pace.

Through research and conversations, we discovered many investors are confused about how to get going on a deal with little to no money. So, we’ve taken a step back and tried to figure out why that is.

We found out many investors don’t understand the power of the appraisal/ARV. When you get into a long-term loan, you get to use the appraisal value/ARV. It doesn’t matter what you originally paid for the property or the amount of money you put in to fix it up. As long as you set up the loan properly, then you should be able to use the appraised value/ARV.

If you’re ready to maximize your cash flow, capture lots of free equity, and live the life you want, check out the full video.

Want more videos with more tips to maximize your cash flow? Subscribe to our new YouTube channel!

So far this week, all evidence is pointing towards increasing stability and improvements on the conventional mortgage front.

In short: conventional mortgage interest rates are really good. But what does that mean for you?

Let’s face it: as rates drop, the question of whether or not to refinance runs through all our minds.

Would you like to find out (without the sales pitch from your mortgage person?)

Anyone can crunch the numbers in just a few minutes with just a few items.

Yes. It involves math. But we swear it’s EASY.

For now, all you need is a piece a paper, a pen, a calculator, and your mortgage information. (You can pull this info directly from your mortgage company’s website). Then, follow these three steps:

Step 1: Locate the amount you pay monthly for principal and interest. (Ignore everything but your principal and interest (i.e. taxes and insurance).

Step 2: Locate the number of months remaining on your loan.

Step 3: Multiply your monthly payment by the number of months you have left on your loan.

That’s it!

Let’s look at an example:

A: Your monthly principal and interest payment is $1,200.

B: You have 288 payments left on your loan.

C: $1,200.00 X 288 = $345,600

(Scary sometimes to see how much you really owe, isn’t it? Don’t panic.)

Now, let’s say that you have an opportunity to refinance and lower your interest rate with a new payment of $1,100. Should you do it?

On your new loan, you’d pay $1,100.00 for 30 years (or 360 months). That’s $1,100.00 x 360 = $396,000.00

If you refinance, you’d increase your monthly cash flow $100.00. However, as a result, you’d pay an extra $50,400.00 over the life of your loan!

So, is the extra $100/month worth an extra 72 months (6 years) of mortgage payments? Does refinancing make sense for you financially? Well, that’s up to you.

Perhaps cash flow is more important at this time in your business life and paying the extra years is ok with you. That’s a decision only you can make. At least when you know all the numbers, you can make your call an educated one.

Try it on all your loans and find out what makes sense for you!

Your payments __________________ Months remaining _______________

Total remaining to be paid ___________________

Okay, we’re sure a few questions are swimming around in your head, so we’ll see if we can answer some of the most common ones upfront:

Q: “What if I’m not going to keep the property for 24 or 30 years? At what point does it make sense to refinance?”

A: That’s coming up in the next article.

Q: “What if I want to use those savings and pay down my mortgage?”

A: We’ll be addressing that in a future article as well.

Q: “What is my breakeven interest rate?”

A: There are so many paths you can go down and we’ll cover as many as we can. We’ll also provide a tool for you to run all these scenarios.

Want an investor tool that can run these numbers (plus your breakeven rate and many more) in seconds? We have one in the works. Just get on our contact list, and we’ll let you know when it’s ready!

By knowing these numbers, you can save tens of thousands on each refinance.

Don’t worry if math isn’t your “thing.” If you don’t feel like doing this or worry the math might overwhelm you, we’ve got your back. Shoot us an email with your current statement and we can run them for you.

The Difference Between Cash Flow and Profits

Did you know there’s a difference between cash flow and profits? Actually, there’s a significant difference.

Cash flow is the money flowing in and out of your bank account every month to fuel a project from start to finish. The trick is to match incoming money to outgoing money. If cash flow is negative, you’ll spend more time juggling who gets paid and how instead of focusing on finishing and selling the project.

Profits are what you make after everything is paid. Basically, they’re the BIG payday at the end of a project. Profits replenish the pool of money you get to play with, apply toward your next project, and use to lower costs on your next deal. They can also help your cash flow by showing lenders you’re worthy of better products and rates. In their eyes, you’re successful and able to repay them.

Ready to boost your cash flow AND profits? Then contact us!

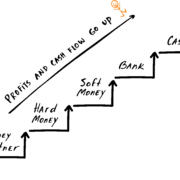

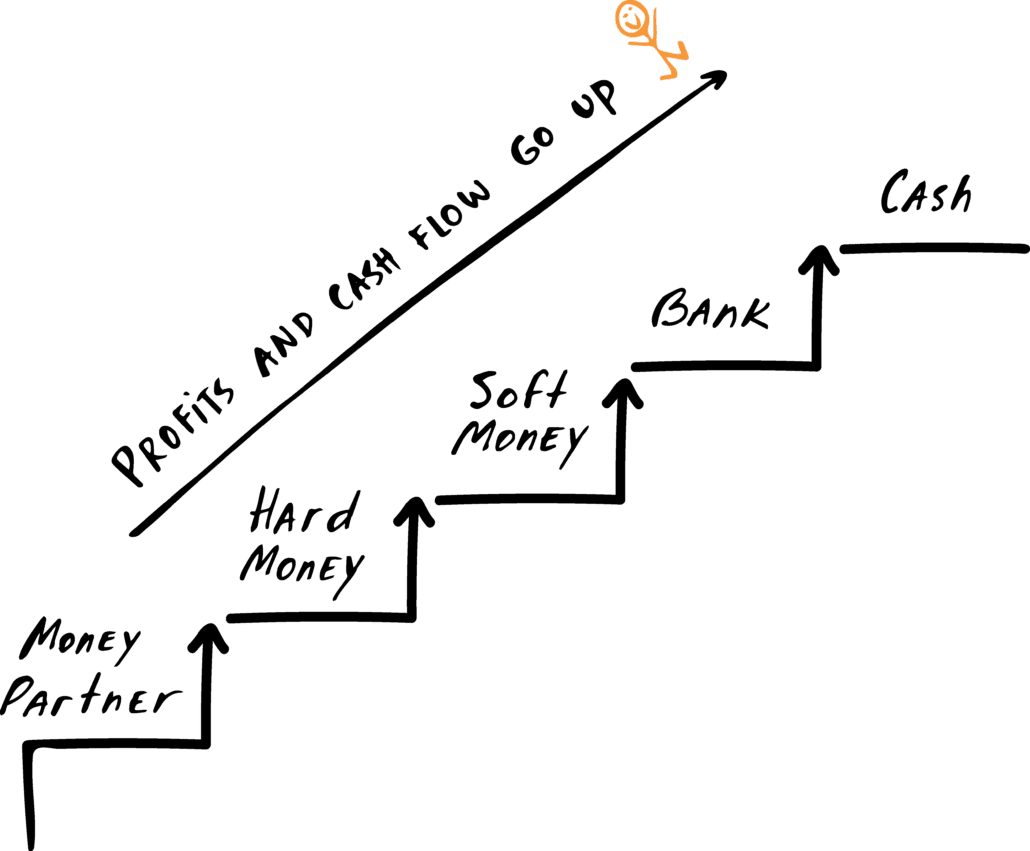

Now that you’ve seen the benefits of the Fix and Flip Escalator, let’s talk about what you can do to take advantage of it!

By moving away from an expensive partner and heading toward profit boosting cash, you’re sure to make A LOT more money A LOT faster.

Which means you can start fulfilling all of your lifelong dreams sooner.

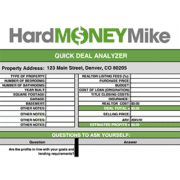

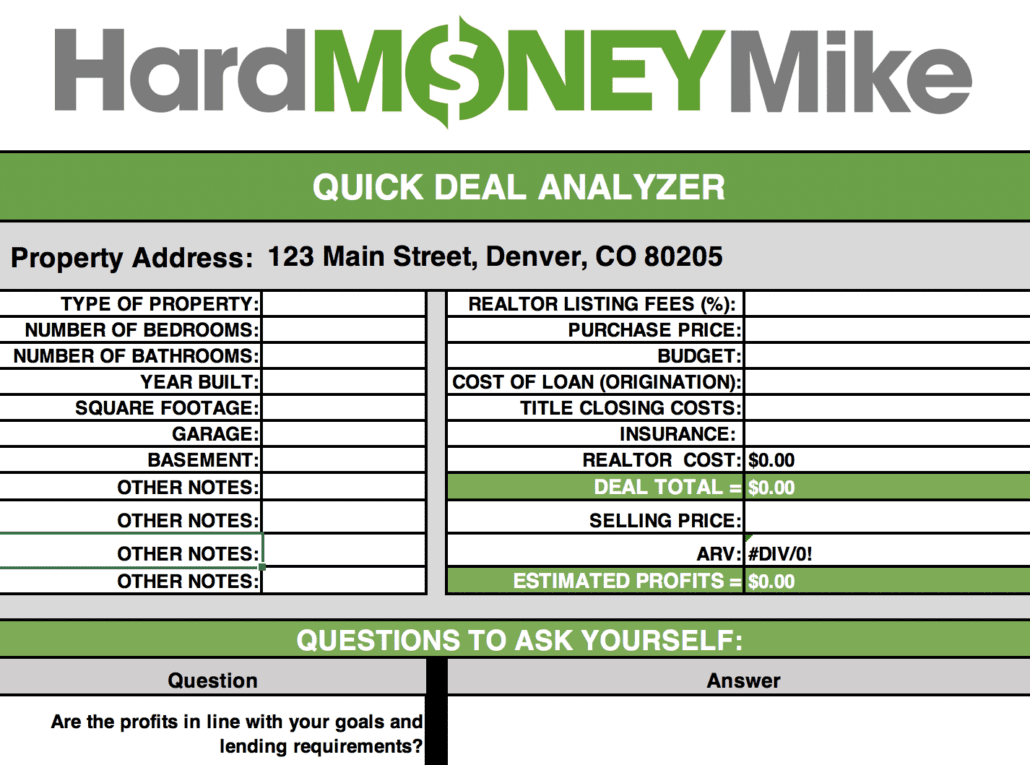

Introducing the new Quick Deal Analyzer from Hard Money Mike!

With the Quick Deal Analyzer, you’ll be able to find out:

If you’re interested in making more money on your next deal, download the Quick Deal Analyzer here.

Looking for a powerful tool to analyze the financing of your next project? Then check out our new explainer about the Loan Optimizer!

If you’re ready to download this beneficial tool, click here.

When you use the Fix and Flip Escalator, you’ll quickly realize it’s not magic. It’s SIMPLE math.

This week, let’s use the escalator to see what your money does when you complete four deals per year.

Hard Money > Soft Money

Profits increase by $12,000

$12,000 x 4 deals = $48,000

Hop up another step to bank financing, and this happens:

Hard Money > Banking

Profits increase by $17,000

$17,000 x 4 deals = $68,000

Then look at how your profits skyrocket over the course of two years:

Hard Money > Soft Money

$48,000 x 2 years = $96,000

Hard Money > Banking

$68,000 x 2 years = $136,000

You know what these numbers mean, right? Yes, instead of losing $136,000, you’re making $136,000. That’s money you can reinvest or spend on…anything! Hey, it’s your money. You can do whatever you want with it.

Are you ready to hop on the escalator yet? If so, contact us!

Introducing the new Quick Deal Analyzer from Hard Money Mike!

With the Quick Deal Analyzer, you’ll be able to find out:

If you’re interested in making more money on your next deal, download the Quick Deal Analyzer here.