What number is a good credit score goal for real estate investors?

Credit scores range from the 400s to 800s. But for the purposes of the lending world, that range shrinks to the mid-600s to upper-800s.

Over the past 6 months, with inflation and interest rates rising, big institution lenders have tightened their grip on loans. Not just anyone can get a loan – you’ve got to have a good score.

But what is a good credit score for real estate lenders?

Changing Definition of a Good Credit Score

Before this recent shift in the economy, the lowest score considered by a lender was 640. Now, most lenders won’t look at anyone under 680. And that 680 minimum could soon turn into 720.

Institutions raise credit score minimum requirements to cut investors from the loan pool. This means many of your competitors will be unable to find the same kind of money they could 6 months ago.

You don’t need to be one of the investors squeezed out of the lending space. But you’ll need to understand exactly where your credit is, how to improve it, and what range lenders will be looking for.

Make sure you’re credit-ready for these upcoming opportunities.

https://hardmoneymike.com/wp-content/uploads/2022/07/what-is-good-credit.png6811048Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-07-25 12:00:432022-07-25 19:40:16What is a Good Credit Score?

Because we care about our clients and anyone else who decides to invest in real estate.

So, here’s the brutal truth: there are people who will lie to you in this industry. Lenders, realtors, other investors, and so on. Or only tell you half-truths.

I know. This is a HUGE surprise.

Okay, maybe not.

But, even if common sense and experience tells you that people lie, you can’t always believe it when it happens to you.

Why?

Because, more often than naught, you WANT something to be true, especially when it comes to making money. You want to believe you found an incredible deal, or an incredible lender, or an incredible something that nobody else has had the luck to find.

We all want those incredible moments to be true, right?

First, if it seems too good to be true, it probably is.

For example, “If you buy this property, then you can generate $5,000 – $6,000 every month.”

Okay, that’s definitely a red flag.

Sure, we all want to make excellent cash flow on our properties. But, even in our competitive market, it’s near impossible to make $5,000-$6,000 every month on a standard rental in most towns or cities. The norm is more like $200-$500 a month…at least until a property pays off.

But, even then, making $5,000 – $6,000 every month with a single property is…too good to be true.

Unfortunately, we’ve seen this situation happen more than once to our investors. They get convinced of a sweet, sweet deal and jump into it. And…it doesn’t take long for them to figure out the person who convinced them to buy the property streeetched the numbers and the truth…a lot.

So, what can you do when a red flag waves in your face?

Ask questions.

Okay, someone told you something that’s too good to be true. Now what?

That’s right: ask questions. A lot of them!

For example, let’s say a lender quotes you a 4% rate when everyone else is quoting you about 10%.

Your first reaction is to cheer and think, “That’s amazing! I’m so happy I called this lender.”

But your second reaction should be, “Wait, why? Why is this lender quoting me so much lower than everyone else? What do they see that the other lenders missed? Why are they so much more forgiving and accepting of my financial history?”

There’s gotta be a catch.

Trust us, there is.

When lenders give quotes that are significantly lower than their competitors, it’s because they pad the rest of the loan with junk fees. They charge for everything, not just the loan itself. So, before you know it, you’ll be paying more than the 10% interest you would’ve paid with one of the other legitimate, honest lenders.

So always ask questions when a red flag pops up.

And, part of that process includes…

Getting a second opinion.

So, a red flag went up. Then you asked the lender, realtor, seller, investor, or whoever a bunch of follow-up questions to figure out if they’re telling you the truth…or yanking your chain and taking advantage of you.

Sadly, even if you grill this person, you might not get a direct or honest answer from them.

So, go and get a second opinion. Heck, get a third opinion! There are plenty of experts in the field to ask. Go out and see what they think of this “too-good-to-be-true” offer. Is it real…or fake?

Spoiler alert: it’s probably fake.

By taking these simple steps, you can protect yourself and your wallet from falling into a bad situation.

Just remember:

If it’s too good to be true, ask questions and then get a second, third, or even fourth opinion. Do your due diligence to save yourself a lot of hassle…and money.

Happy investing!

https://hardmoneymike.com/wp-content/uploads/2022/02/How-to-Combat-Red-Flags-in-Real-Estate.jpg267800Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2022-02-14 10:00:242022-06-18 14:16:473 Ways to Combat Real Estate Red Flags

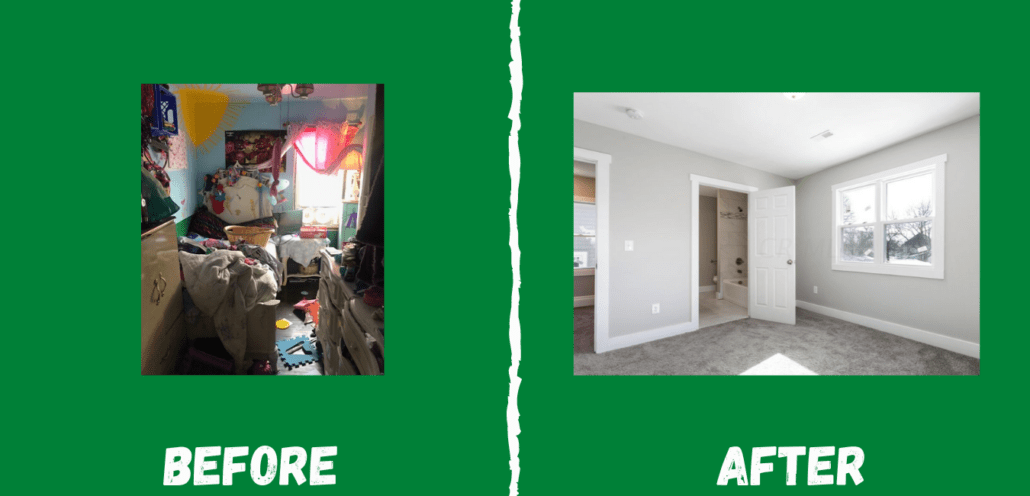

Today’s Before and After Spotlight is a fantastic fix and flip property that one of our repeat clients in Ohio completed.

The whole team at Hard Money Mike thinks he did a wonderful job. He transformed an eyesore into a moneymaker for himself and the rest of the neighborhood.

This property is a shining example of what the real estate investing community is all about.

Check out the fix and flip transformation for yourself!

We’re a Colorado-based lender who lends money on all types of commercial/value-add properties. So, whether you want to invest in fix and flips, rentals, land, or wholetailing, we can discuss your funding options. We even offer bridge loans for those who need to close a financial gap.

Happy investing!

https://hardmoneymike.com/wp-content/uploads/2020/07/6-2.png12602240Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2021-08-17 15:30:282021-08-19 15:55:14Ohio Fix and Flip: Before and After Spotlight

Close your eyes. Clear your mind. Take a deep breath.

Now, let’s pretend we’re talking to each other two years from now. What happened during that time period that made you proud and put a smile on your face? How does your cash flow look? What kind of work schedule do you have? How does life look for you and your family?

When it comes to investing, we have discovered that thinking ahead two years leads to the most success. Why two years? Well, it’s short enough to imagine without being overwhelming, and it’s long enough to create tangible, positive change in your life.

Coming up with a plan is as easy as one, two, three:

Step 1: Imagine where you want to be in two years.

Step 2: Evaluate where you’re starting at today.

Step 3: Create a plan that connects your current reality to your future dreams.

How do you formulate an actual plan? Well, that’s what our team is here to help you do. It’s just a matter of picking up the phone and giving us a call to chat.

One conversation can change your future…and your life!

https://hardmoneymike.com/wp-content/uploads/2019/07/backlit-clouds-dawn-415380.jpg14402160Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2021-05-26 10:00:422021-05-20 09:46:50What’s Your 2-Year Plan?

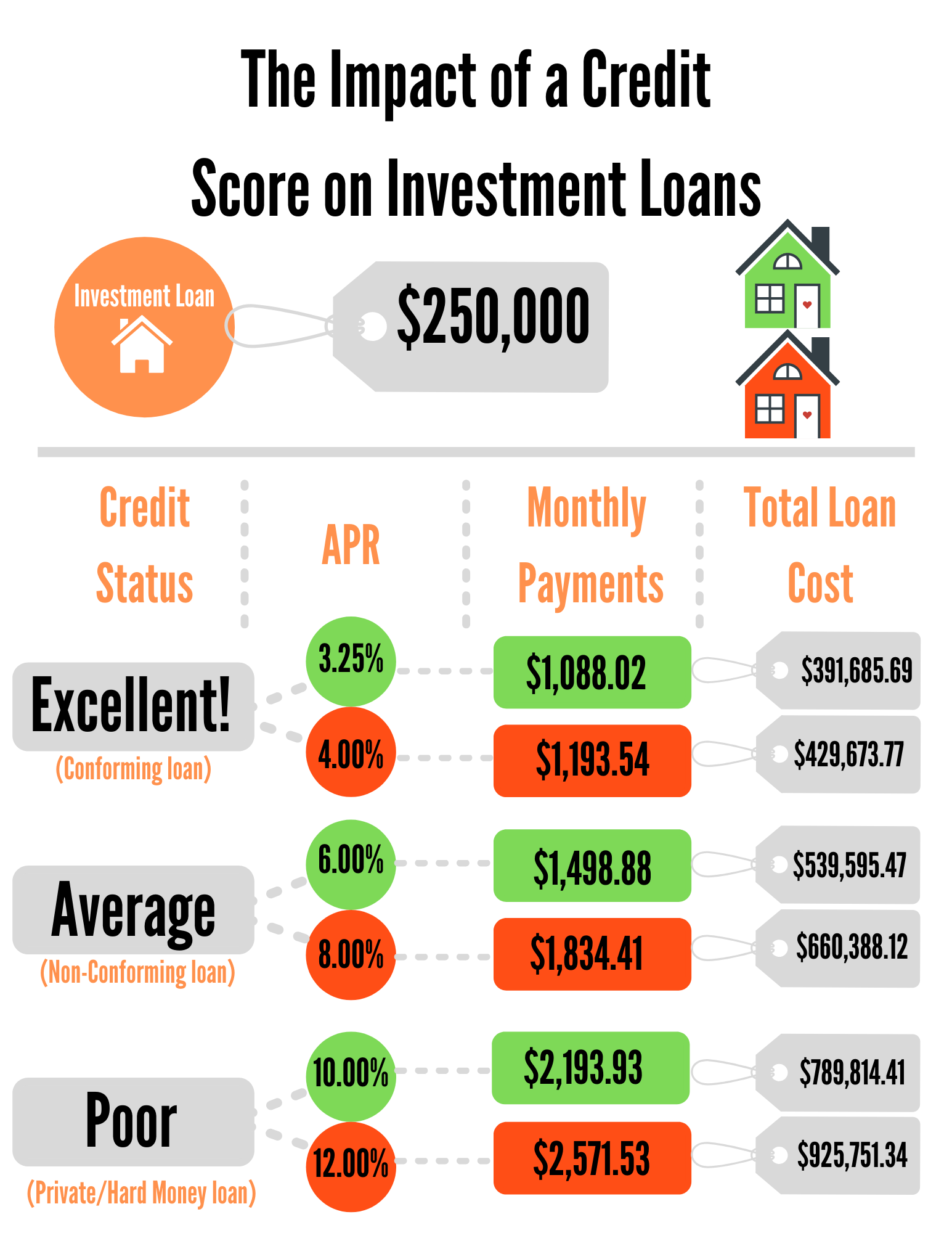

How much money might a lackluster credit score be costing you over the life of your investment business?

You probably hear a lot of talk in the mortgage industry about your credit score and the effect it can have on your interest rates, but do you really have an idea of how much it’s affecting your bottom dollar?

Do you know how to determine your Return on Credit (ROC)?

Can you crunch the numbers to figure out how much your score is helping your cash-flow? How about how much money it’s sucking out every month?)

These calculations can get complicated, but the takeaway here is that a less-than-stellar score can really be costing your tens of thousands of dollars over the lifetime of your loan. And when your loan is on investment property, (or several,) you may as well be lighting your profits on fire.

We want to help! Contact our team so we can help you see where you’re currently at, and where you could be going instead.

Let’s get you to your goals faster by trimming some of the fat from your financing!

Hard Money Mike is a lender based in Colorado offering services in several states. We lend money for all varieties of commercial-based properties. So whether you’re trying to finance a fix-and-flip, vacant land, whole-tailing, or looking for a builder bridge loan, we’ve got you covered.

Call Mike Bonn at: 303-539-3000 or email Mike@HardMoneyMike.com

https://hardmoneymike.com/wp-content/uploads/2021/03/credit-score-eating-profit-img.jpg6671000Mike Bhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngMike B2021-03-24 12:50:112022-01-19 11:02:34What is your credit score costing you?

https://hardmoneymike.com/wp-content/uploads/2020/11/Screen-Shot-2020-11-23-at-2.44.26-PM.png696740Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2020-11-23 15:47:342020-11-23 15:47:34Good information about the question on every investors mind.

Hard Money Mike does business differently than most others in the industry. Our #1 goal is to HELP YOU.

Truly. It’s as simple as that.

We want to BOOST your cashflow, find the very best products for your specific projects, and place you in a solid financial position.

We also strive to move at the speed of light.

What does that mean, exactly? Well, it means we can close most deals in DAYS, not weeks. Our team works efficiently and effectively to dot all I’s and cross all T’s to ensure you sign the dotted line as soon as possible.

No more sweating bullets as you wait weeks (or even months) to close a deal. With us, you can often close within a week!

https://hardmoneymike.com/wp-content/uploads/2019/08/Money-In.png21831624Jenna Weldonhttps://hardmoneymike.com/wp-content/uploads/2019/06/hard-money-mike-logo.pngJenna Weldon2020-09-03 09:00:542020-08-25 10:00:39How Hard Money Mike Does Business: FAST!

Rates on the conventional side have maintained strong with rates in the low 3’s. If you’re still wondering whether or not you should refinance, we’re going to dive into what we call ‘The Tipping Point Rate.’

This week, we’re seeing more larger non-conventional companies dipping their toes back into the investor loan water. This gentle ease back in helps increase liquidity, but it still comes at a price: Lower LTVs and higher costs.

What This Means for You:

There is an exact rate where it’s wise to refinance. We call this ‘The Tipping Point Rate.’ This specific rate is the point where you won’t pay a penny more in principal and interest over the life of the loan.

Going above this point might increase your cash flow, but it will end up costing you more in the long run. Sometimes this means it’s better to stick with what you have now. We’re focused on putting more money in your pocket and less in the bank’s pocket.

This is for investors looking to increase monthly cash flow without adding lifetime cost of debt. So, if you’re solely concerned about your monthly cash flow, this probably isn’t the program for you.

So how does this work? Let’s take a look at an example.

Joe is an investor who is looking at refinancing to increase his cash flow every month. But not if it means paying tens of thousands of dollars extra to the bank in principal and interest.

Joe has been paying his current mortgage for 5 years. If he keeps the loan until it’s paid in full, he’ll end up paying $360k in payments over the next 25 years.

Joe wants to know the exact rate that he can refinance to a new 30-year fixed without increasing his amount owed. If it exceeds $360k, then he won’t refinance.

By knowing this exact rate, he can stretch his payments out and lower his interest rate without paying a penny more over the life of the loan.

How do we find Joe’s Tipping Point Rate?

Luckily, we have a handy program that can calculate just that. If you would like to know your own Tipping Point Rate, send us an email! We’ll run the report specifically for you and your property!

Note: Investor Real Estate Loans doesn’t currently lend in all states, but we are always happy to help and make sure you understand your numbers!

*All non-commercial and construction loans offered by TNS Loans NMLS #1719349

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.