Hard Money: The Out-of-the-Box Loan Real Estate Investors Need

/in Beginners, Finance Tools, Fix-and-Flips, Gap Funding, Lending Options, Resources, Tips, Wholesale DealReal estate investing is full of deals that don’t fit the normal rules. However, that’s often where the best opportunities are found. That’s why understanding Hard Money: The Out-of-the-Box Loan Real Estate Investors Need can change how you look at funding. Instead of getting stuck when a deal doesn’t fit the bank’s box, you can move forward with speed, flexibility, and confidence.

What Is Hard Money?

When real estate investors talk about hard money, they are talking about out-of-the-box lending. So, what does that really mean? Most loans today come from big lenders. However, those lenders work inside a tight box. They want perfect deals, clean properties, strong credit, and clear history. But here’s the problem—not every great deal fits in that box. That’s where hard money comes in, and because of that, investors can move forward when others get stuck.

“In-the-Box” vs “Out-of-the-Box” Lending

In-the-Box Lending (Traditional Loans)

Most lenders want a simple and safe deal. For example, they prefer a single-family home, sometimes up to 3–4 units. In addition, they want a credit score over 700, past experience, and money into the deal. Also, they look for strong comparable sales nearby. So, in short, they want everything to fit neatly into their system.

Out-of-the-Box Lending (Hard Money)

On the other hand, hard money looks at deals in a different way. Instead of asking, “Does this fit our rules?” they ask, “Does this deal make sense?” Because of that, hard money can fund deals that others won’t, and that is why it plays such a key role for investors.

Why Investors Need Hard Money

Real estate is not always clean and easy. In fact, many of the best deals are messy, unusual, or time-sensitive. So, if you only rely on traditional loans, you will miss out. However, when you use hard money, you gain speed, flexibility, and opportunity. More importantly, you gain control over your deals, which helps you move faster and make better decisions.

Real Examples of Out-of-the-Box Deals

Let’s make this simple. Here are a few real-world examples that show how hard money works.

Example 1: Quick Flip (2–4 Weeks)

Sometimes, you find a deal you don’t want to fully rehab. Instead, you clean it up, list it fast, and sell it quickly. Traditional lenders usually won’t touch this type of deal. However, hard money can step in, and because of that, you can move quickly and lock in profits.

Example 2: Double Closing (Wholesale with Ownership)

In some deals, you buy the property first and then sell it to another buyer. This is called a double closing. Now, many lenders won’t allow this structure. But again, hard money can step in and help you complete the deal smoothly.

Example 3: Land Deal

Here’s a simple example. You buy land for $300,000, then you split it into 8 lots, and after that, you sell each one for $75,000 to $100,000. That creates strong profit potential. However, most lenders will say no to this type of deal. Meanwhile, hard money sees the opportunity and focuses on the upside.

Example 4: Small Town Property

Many lenders avoid small towns because there are fewer sales and fewer comparable properties. Because of that, they feel the deal is too risky. However, some of the best deals live in small towns, and hard money works well in these areas. So, instead of missing out, you can move forward with confidence.

Example 5: Finish a Project Loan

Let’s say you are 80% done with a project, but then you run out of money. Now, the project slows down, and as a result, your profit starts to shrink. However, hard money can step in, fund the remaining work, and help you reach the finish line faster.

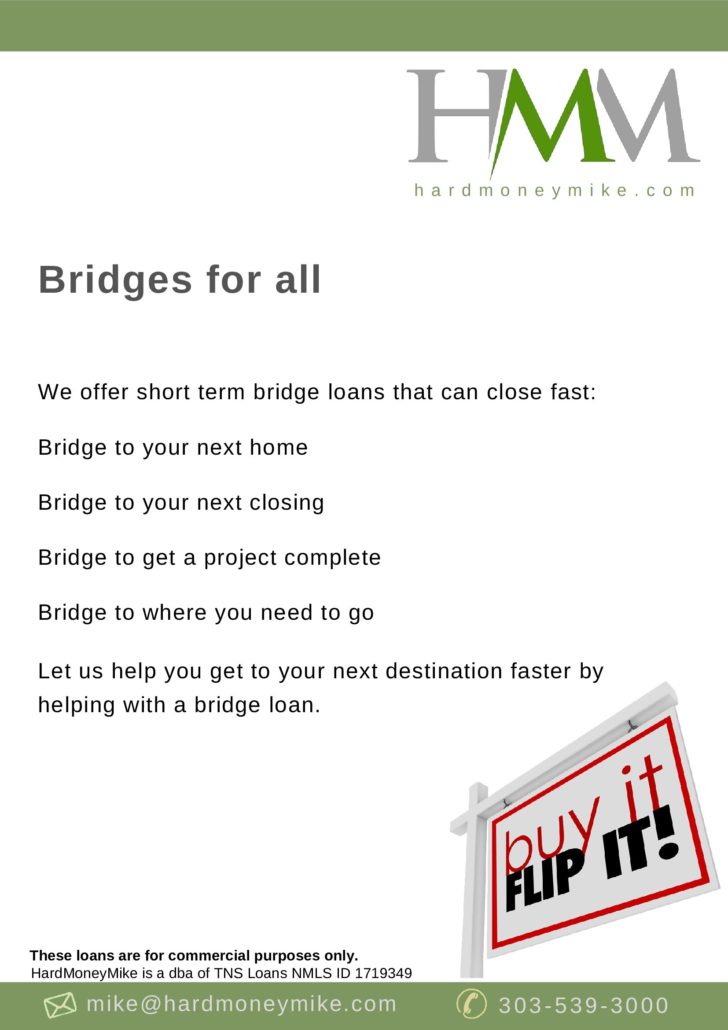

Example 6: Bridge Loan

Sometimes, you need to buy a new property while selling another one. That’s where a bridge loan helps. It allows you to move forward without waiting, and then once your old property sells, the loan is paid off. Because of that, you keep your deals moving instead of getting stuck.

What Hard Money Really Cares About

This is where things get simple. Hard money is not focused on perfection. Instead, it focuses on the deal, the exit plan, and the opportunity. In other words, does the property have value, can you sell or refinance it, and is there profit and equity? If those three pieces work together, then the deal can work, and that is what really matters.

What Hard Money Does NOT Focus On

Unlike traditional lenders, hard money is more flexible. For example, your credit score matters less, your experience is not always required, and your income is not the main focus. Instead, the deal leads the way. Because of that, even a first-time investor can succeed if they find the right opportunity.

Why This Matters for Your Profits

Here’s the truth most investors miss—the best deals are often the hardest to fund. So, if you only use traditional loans, you move slower, miss deals, and lose profits. However, when you add hard money to your strategy, you move faster, close more deals, and increase your profits. As a result, you create more opportunities over time.

Simple Story to Bring It Together

Think about this like driving across town. If you have full funding, it’s like hitting every green light. On the other hand, if you have some funding, it’s like hitting every other light. And if you don’t have funding, it’s like hitting every red light and sitting in traffic. So, who gets there first? More importantly, who makes more money?

When Should You Use Hard Money?

You should use hard money when the deal does not fit the normal box, when you need speed, when you need flexibility, or when you see a strong profit opportunity. Because at the end of the day, if the deal makes sense, hard money can help you make it happen.

Final Thought

Real estate investing is not about perfect deals. Instead, it is about finding good deals and having the right funding to close them. So, don’t let the “box” limit your success. Because when you think outside the box, that is where the real profits live.

Next Step

If you have a deal that feels a little different, that might be your best deal. So, take a second look, run your numbers, and get a second set of eyes. Because the right funding can turn a “maybe” deal into a real profit.

Watch our most recent video to find out more about: Hard Money: The Out-of-the-Box Loan Real Estate Investors Need