Top 5 Questions to Ask Hard Money Lenders

Today we are going to discuss the top 5 questions to ask hard money lenders before you get a loan. Not all hard money lenders are the same. That’s why asking the right questions before you sign is key. Whether you’re doing a flip, a BRRRR, or a bridge loan, these five questions can save you time, stress, and a whole lot of money.

1. What Are Your Total Costs?

Don’t just look at the interest rate. Lenders can make their deals sound great by hiding extra fees.

👉 Some charge low interest, like 10%, but add in:

-

2 points (That’s 2% of the loan upfront!)

-

$1,000 in processing fees

Let’s break that down:

-

Loan Amount: $200,000

-

2 Points: $4,000

-

Six Months of Interest at 10%: $10,000

-

Processing Fee: $1,000

-

Total: $15,000

Now compare it to another lender:

-

Interest Rate: 12%

-

No Points

-

But $4,000 in other fees

-

Six Months of Interest at 12%: $12,000

-

Total: $16,000

👉 Even with no points, the second lender costs more.

💡 Use a tool like the Loan Cost Optimizer at hardmoneymike.com to compare lenders side-by-side.

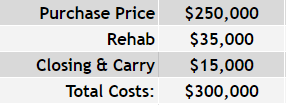

2. How Do You Decide Loan Amounts?

Lenders calculate what they’ll lend based on different values. Some use just the purchase price, others use ARV (After Repair Value).

Let’s look at two examples:

-

Purchase Price: $150,000

-

Rehab Costs: $50,000

-

ARV: $300,000

One lender might only give you 75% of the purchase price, or about $112,500.

Another lender might lend based on ARV, offering:

-

90% of the purchase = $135,000

-

100% of the rehab = $50,000

-

Total Loan: $185,000

👉 That’s a huge difference. Ask if they use purchase price or ARV to calculate your loan.

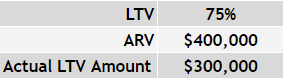

3. How Do You Decide Property Value?

This one’s big. Some lenders use real appraisers. Others use in-house tools or AI. The problem? They can value your property way lower than what it’s actually worth.

Example:

-

One lender values the ARV at $300,000

-

Another comes in at just $250,000

If they lend up to 75%, here’s what you’d get:

-

$300,000 ARV: Loan up to $225,000

-

$250,000 ARV: Loan up to $187,500

👉 That’s almost a $40,000 difference in your funding!

Always ask:

-

Who determines value?

-

Can I provide my own comps?

-

Can I dispute a low value?

4. Are There Prepayment Penalties?

Some lenders sneak in rules like:

-

Minimum interest guarantees

-

3, 6, or 9-month required interest payments

Even if you pay the loan off early, you’re stuck paying interest for those months.

👉 Ask about any minimum interest periods. Make sure the loan fits your timeline.

5. How Do Draws Work?

If you’re doing a flip or a BRRRR, you’ll likely have rehab money held in escrow.

For example:

-

Rehab budget: $50,000

-

That money is held until work is done

-

You’ll get it back in draws (aka stages)

Ask:

-

How fast can I get my draw?

-

Are there fees every time I request one?

-

Do I need an inspection or lien waivers?

👉 If your contractor can’t get paid, they might walk off the job. That’s the last thing you want.

Final Thoughts

These five questions can help you find the best lender for your project:

-

What are the total costs?

-

How is the loan amount calculated?

-

How do you come up with property value?

-

Are there prepayment penalties?

-

How do your draws and escrow work?

✨ Want help comparing lenders? Try the Loan Cost Optimizer at HardMoneyMike.com.

Watch our most recent video to find out more about: Top 5 Questions to Ask Hard Money Lenders BEFORE You Get a Loan