SOS! Stuck in a Fix & Flip—Here’s How to Get Out

SOS! Stuck in a Fix & Flip—Here’s How to Get Out

Today we are going to discuss SOS! Stuck in a Fix & Flip! Flipping houses can feel exciting—until it doesn’t. Sometimes a property just won’t sell for what you need. Stress builds. Bills pile up. And you start asking, what now?

The good news? You still have options. Let’s look at three ways to pivot and move forward.

1. Update It: Bring the Property Up to Market Standards

Buyers today want move-in ready homes. If your property looks unfinished or dated, they’ll move on to the next one.

Ask yourself:

-

Does the home need a new roof?

-

Are the floors worn out?

-

Could a kitchen or bathroom upgrade seal the deal?

-

Is the yard still bare or messy?

👉 Example: If your flip looks great inside but the landscaping is dirt and weeds, buyers might skip it. Spending a little more to finish the yard could push it to the top of the list.

When the market has plenty of choices, your property needs to shine brighter than the rest.

2. Bridge It: Buy More Time with a Short-Term Loan

Sometimes the problem isn’t the property—it’s the timing.

That’s where a bridge loan comes in. It can carry you from your current fix-and-flip loan into the next selling season. Most bridge loans last one to two years.

Before you bridge, check your burn rate:

-

Monthly loan payments

-

Taxes

-

Insurance

-

Utilities

👉 Example: If your property costs $3,000 a month to hold but you still have $50,000 in potential profit, bridging for six months could make sense—especially if rates drop or the market heats up.

But if your margins are too thin, it may be smarter to sell now, take a small hit, and move on. Sometimes limiting your loss is the best business move.

3. Turn It: From Flip to Rental

If selling isn’t working, consider turning the property into a rental.

Options include:

-

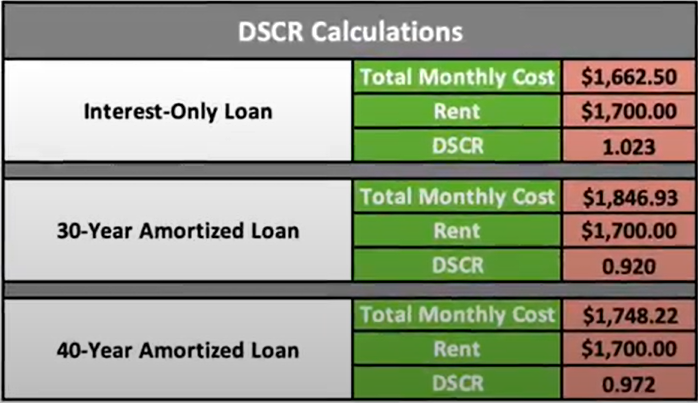

DSCR loan (Debt Service Coverage Ratio loan): Approval is based on rental income, not your personal income.

-

Conventional loan or bank loan: Great if you qualify and want long-term stability.

-

Short-term or mid-term rentals: Could generate strong cash flow depending on the area.

⚠️ Watch your listing price! Lenders often use the lower of the appraisal or listing price. Dropping your list price too low can hurt your refinance options.

👉 Example: One investor kept cutting her list price to $250,000. But when she applied for a DSCR loan, the home appraised at $330,000. Because lenders had to use the lower number, she couldn’t get the funds she needed. Keeping her listing higher would have opened better options.

Turning a flip into a rental might even be the push you need to start building a long-term portfolio. Rentals bring cash flow, tax benefits, and future wealth.

The Bottom Line

Every stuck flip has a solution. The key is to:

-

Know your numbers.

-

Check your stress level.

-

Decide whether to update, bridge, or turn.

Real estate is a business. Sometimes it’s about maximizing profit. Other times it’s about limiting loss and keeping momentum.

Need a Second Set of Eyes?

If you’re stuck, don’t stay frozen. A quick strategy session could help you see your best path forward—whether that’s finishing updates, bridging into the next season, or refinancing into a rental loan.

Let’s clear your mind, clear the deck, and get you moving on to your next deal.

Contact us today to find out more!

Watch our most recent video to learn about: SOS! Stuck in a Fix & Flip—Here’s How to Get Out