The Fundamentals of Real Estate Investing: Profit Breakdown

When people first start flipping houses, they often think a lender simply hands them money to buy a property. However, that is not how a fix-and-flip loan works. Instead, money moves through several stages before, during, and after closing. That is why understanding The Fundamentals of Real Estate Investing: Profit Breakdown can help you avoid surprises and make better decisions. More importantly, it helps you plan your cash flow, protect your profits, and keep projects moving forward. Think of a fix-and-flip project like a series of money buckets. Some money comes from the lender. Meanwhile, some money comes from you. As a result, you need to know where every dollar goes before you start a deal.

In this guide, you will learn how funding works, what costs to expect, and how to calculate your real profit at the end of a project.

Understanding the Lender’s Role

Before looking at the numbers, it helps to understand what a lender typically funds. Most fix-and-flip lenders focus on two important numbers:

After Repair Value (ARV)

ARV is the estimated value of the property after all repairs are complete. As a general rule, many lenders want the total project cost to stay at or below 75% of the ARV. Therefore, this number helps protect both the lender and the investor.

For example:

- ARV = $260,000

- 75% of ARV = $195,000

If your purchase and rehab costs stay below $195,000, the deal may fit the lender’s guidelines.

Loan-to-Cost (LTC)

Loan-to-cost measures how much of the project the lender will fund.

For instance, a lender may offer:

- 90% of the purchase price

- 100% of the rehab budget

As a result, the lender may cover most of the project costs, but you still need money available for other expenses.

Furthermore, most fix-and-flip loans are:

- Short-term loans

- Usually 6 to 12 months

- Interest-only payments

- Designed specifically for renovation projects

Because of this, speed matters. The faster you finish and sell the property, the more profit you usually keep.

The Five Stages of Funding

Successful investors understand where money flows during every stage of a deal.

These stages include:

- Pre-Closing

- Closing

- Post-Closing

- Pre-Sale

- Sale and Profit Collection

Let’s look at each stage.

Stage 1: Pre-Closing Costs

Pre-closing happens after you put a property under contract but before you officially buy it. During this stage, several costs may appear.

Earnest Money Deposit

An earnest money deposit shows the seller you are serious about buying the property.

Example:

- Earnest money deposit = $2,000

This money comes from your funds, not the lender’s funds.

Inspection Costs

Some investors order inspections to uncover hidden issues.

For example, an inspection may reveal:

- Plumbing problems

- Foundation issues

- Electrical concerns

- Sewer line damage

Example cost:

- Inspection = $500

Property Valuation or Appraisal

Lenders usually require a valuation before approving the loan.

Example cost:

- Valuation = $600

Total Pre-Closing Costs

In this example:

- Earnest money = $2,000

- Inspection = $500

- Valuation = $600

Total:

$3,100 out of pocket before closing

Therefore, investors need available funds long before the lender provides financing.

Stage 2: Closing Costs

Closing is when ownership officially transfers to you. At this point, both you and the lender bring money to the transaction.

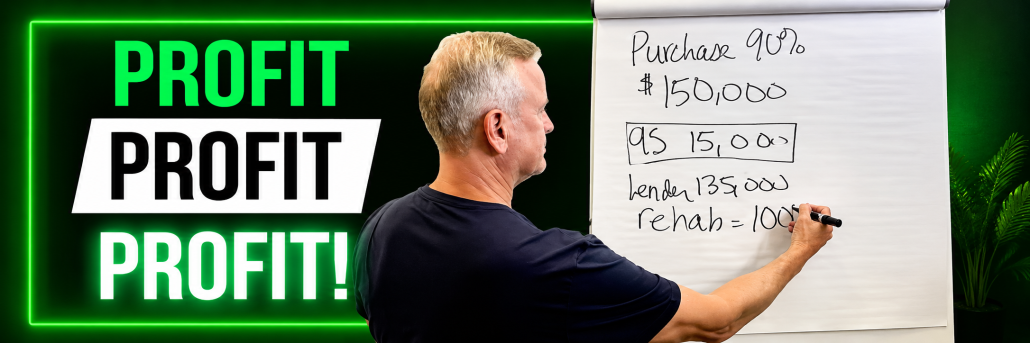

Example Deal

Let’s use the following numbers:

- Purchase price = $150,000

- Rehab budget = $40,000

- ARV = $260,000

Total project cost:

$150,000 + $40,000 = $190,000

Since $190,000 is below the 75% ARV threshold of $195,000, the deal works within the guideline.

Lender Contribution

The lender funds:

- 90% of purchase = $135,000

- 100% of rehab = $40,000

Total loan:

$175,000

Investor Contribution

The investor provides:

- 10% down payment = $15,000

Additional Closing Costs

Besides the down payment, investors often pay:

Loan Costs

These may include:

- Origination fees

- Underwriting fees

- Processing fees

Example:

$5,000

Title and Closing Costs

These costs help ensure clear ownership.

Example:

$3,000

Insurance

Most lenders require insurance before closing.

Example:

$2,000

Total Closing Costs

- Down payment = $15,000

- Loan costs = $5,000

- Title costs = $3,000

- Insurance = $2,000

Total:

$25,000

When combined with pre-closing expenses, the investor has already contributed:

$25,000 + $3,100 = $28,100

Stage 3: Post-Closing Costs

Many new investors overlook this stage. However, these expenses can significantly affect profits.

Rehab Pre-Funding

Sometimes materials must be ordered immediately.

Examples include:

- Windows

- Doors

- Roofing materials

- HVAC systems

- Cabinets

Although the lender may reimburse approved rehab expenses later, investors often pay deposits first. As a result, many investors keep access to:

- 20% to 40% of the rehab budget

In this example:

- Rehab budget = $40,000

- Recommended available funds = $8,000 to $16,000

This money keeps the project moving.

Monthly Carrying Costs

Every month a property remains unsold creates additional expenses.

Common carrying costs include:

- Interest payments

- Utilities

- HOA fees

- Property maintenance

Interest Payment Example

Loan amount:

$175,000

Interest rate:

10%

Annual interest:

$17,500

Monthly interest:

$17,500 ÷ 12 = approximately $1,460

Utilities

Example:

$340 per month

Total monthly carrying cost:

$1,460 + $340 = $1,800

If the project lasts four months:

$1,800 × 4 = $7,200

Therefore, delays directly reduce profits.

Why Speed Matters in Real Estate Investing

Every extra month costs money. For example, if a project drags on for six more months, carrying costs continue to grow. Meanwhile, stress often increases.

Because of this, experienced investors focus on:

- Fast renovations

- Quick decision-making

- Strong contractor management

- Proper funding preparation

Simply put, speed protects profit.

Stage 4: Preparing to Sell

Before listing the property, investors often spend money on final touches.

These costs may include:

- Cleaning

- Photography

- Landscaping

- Staging

- Minor repairs

Although these costs seem small, they can improve buyer interest and help properties sell faster. As a result, many investors view these expenses as investments rather than costs.

Stage 5: Selling the Property and Calculating Profit

Now let’s follow the money all the way to the finish line.

Sale Price

The renovated property sells for:

$260,000

Selling Expenses

Common selling costs include:

- Agent commissions

- Title fees

- Transfer taxes

After these expenses, the investor receives approximately:

$247,000

Pay Off the Loan

The lender receives:

- Principal balance = $175,000

- Remaining interest and fees = $1,000

Total payoff:

$176,000

Remaining Funds

$247,000 − $176,000 = $71,000

At first glance, it may seem like a $71,000 profit.

However, there is one more step.

Subtract Your Cash Investment

Earlier, the investor contributed:

- Pre-closing costs

- Closing costs

- Carrying costs

Total investment:

$35,300

Now subtract that amount:

$71,000 − $35,300 = $35,700

Final Net Profit

$35,700

This is the money left after all project expenses and loan obligations are paid.

What Is a Good Fix-and-Flip Profit?

Many investors aim for a net profit equal to roughly 10% to 15% of the ARV.

Using the example above:

- ARV = $260,000

- Target profit range = $26,000 to $39,000

The example profit of $35,700 falls within that target range. Therefore, the deal produces a healthy return.

Key Lessons from The Fundamentals of Real Estate Investing: Profit Breakdown

Successful investors understand more than just purchase prices. They also understand cash flow. As you evaluate deals, remember these lessons:

- Budget for pre-closing costs.

- Plan for closing expenses.

- Prepare for monthly carrying costs.

- Keep funds available for rehab deposits.

- Track every dollar invested.

- Focus on speed whenever possible.

- Calculate net profit instead of gross profit.

Most importantly, treat every project like a business. When you understand where the money goes, you can make smarter decisions and avoid costly surprises.

Conclusion

The biggest mistake many new investors make is focusing only on the purchase price and sale price. However, real profit comes from understanding every stage of the funding process.

That is why The Fundamentals of Real Estate Investing: Profit Breakdown matters so much. When you understand pre-closing costs, closing costs, carrying costs, lender requirements, and profit calculations, you can approach each deal with confidence.

Furthermore, proper planning helps projects move faster. As a result, you can protect your margins, reduce stress, and build a stronger real estate investing business over time.

Watch our most recent video about: The Fundamentals of Real Estate Investing: Profit Breakdown

")

Leave a Reply

Want to join the discussion?Feel free to contribute!