How Does Your Credit Score Impact Your Cash Flow?

Rates and cash flow depend on your credit score. Here’s just how much:

Let’s look at an example with real numbers to get a picture of just how seriously your can credit score impact cash flow on your real estate investments.

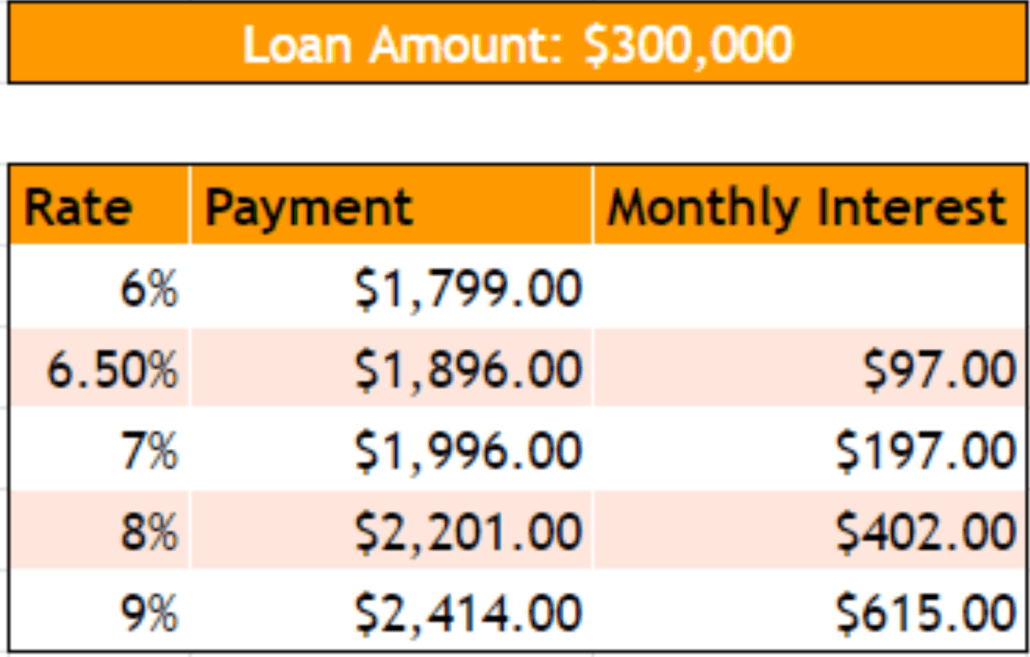

Comparing Interest Rates

Pretend you have a $300,000 loan. And you were able to get a 6% interest rate – a normal rate for today. Your monthly payment would be around $1,800.

But, for every 10 to 20 points your credit score lowers, your rate increases. This raises your monthly payments by $100 to $200.

So with a low score, you’d only be able to get a 9% rate on that $300,000 loan. You’d be giving $615 every month straight to the bank. That’s money other investors will be able to use to re-invest.

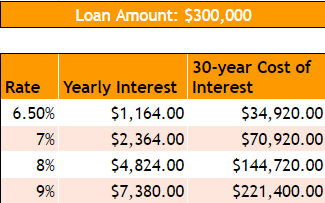

Interest Rates Over the Life of the Loan

This interest story gets worse when we consider the full life of the loan.

The person with a 6.5% interest rate pays a little under $1,200 per year in interest, or around $35,000 for the full 30-year loan.

The person with 9% pays over $7,300 yearly, and over $221,000 over the course of the loan!

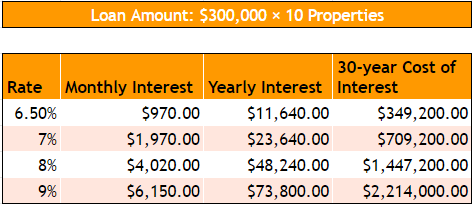

We can take this example out further.

Let’s say we have a portfolio of 10 properties, not just one, each with $300,000 loans.

At 6.5%, you’ll spend almost $350,000 over 30 years between the interest of all the loans. At 9%, you’d pay $73,800 per year on interest alone for your portfolio. As a result, you’d shell out a grand total of $2.2 million in interest in 30 years.

Cash Flow & Credit Score Conclusion

As you can see, a low credit score is a major disadvantage. Properties that would cash flow for someone else, won’t for you. Your debt-to-income could disqualify you for DSCR loans. Your score itself can disqualify you for many other loans.

Look at the impact of your credit score on cash flow. Keep more money to do what you love and give less to the banks in the form of interest.

Above all other investment goals: raise your credit score.

If you need to work with a credit specialist to get everything in line, it’ll be worth your time. Do it ASAP – now is the time to get prepared as a real estate investor. Because in 2023, prices will come down, and you don’t want to miss those opportunities.

Read the full article here.

Watch the video here:

https://youtu.be/sa9iCDxJFnk

")

Leave a Reply

Want to join the discussion?Feel free to contribute!