Why Banks Say No to Real Estate Investors

Why Banks Say No to Real Estate Investors

Why are banks saying no to real estate investors and turning away more business loans? The answer to both of these questions is that there is less money out there. This shrinking pool of money has created a new reality for real estate investors. Unfortunately the money is no longer looking for you, but instead you have to go out and look for it. In further investigating why banks are lending less, what’s available, and where you can find it, investors can make a plan to succeed.

Why are the banks lending less?

First, Banks lend off of assets

Assets are capital plus deposits. The Fed allows banks to take a multiple of 10, 20, or even more times the original amount. The more assets a bank has, the more they can then in turn lend out. More people are moving money out of the banks and into government bonds. These bonds are backed by the government and often have a higher interest rate than what the banks are paying. Banks are seeing their deposits shrink dramatically, thus decreasing the amount of money they are legally allowed to lend.

Second, Reserves for loans in default

The Fed also requires all banks to put money aside for defaulted loans. The more loans that they have in default, or ones who could potentially default, the more money the banks have to put aside. By setting money aside, the banks are not able to lend out money, let alone multiples.

What’s happening inside these banks?

First, Receiving less than paying out

To put it briefly, savings accounts and CD’s that were booked years ago at low percentages are experiencing a dramatic increase. What started at a monthly profit of 3% to 4%, has become a deficit of 5% to 5.25%. For this reason, investors are now upside-down on their assets.

Second, More Notes Maturing

Now, the notes that banks wrote 3 to 5 years ago are now coming due. What started at 3%- 4% interest rates, has skyrocketed to 8%-10%. As you can see, lending is no longer in the forefront of banks’ minds in the traditional sense.

In summery

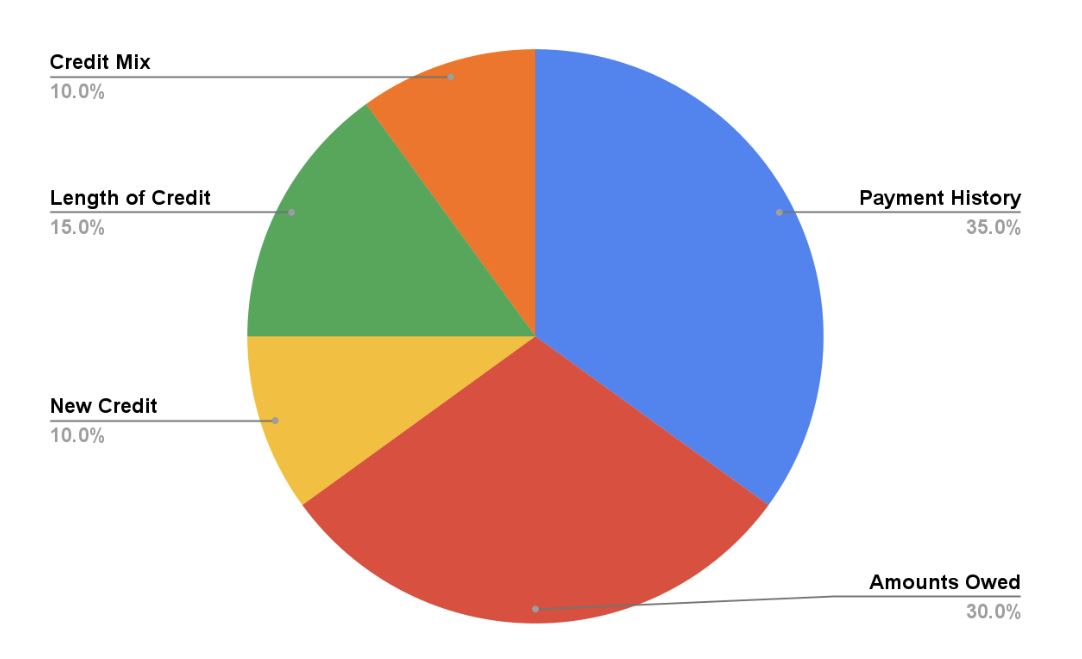

We have deposits leaving the banks, we have loans that are now upside down, and people can no longer qualify. All of these factors combined shrink the funds that banks have available for business owners, for flippers, and for people buying rental properties. With less money available, banks begin their journey upstream to find the “best of the best.” They are looking for people who are bringing in deposits, have good credit scores, and most importantly, they have money for reserves and low loan to value.

What can investors do about it?

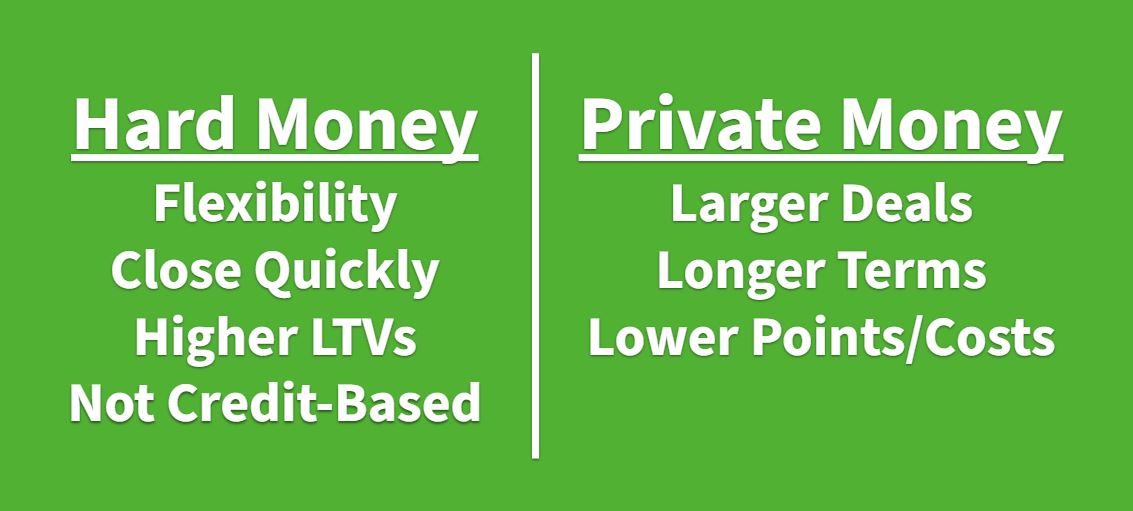

More clients are leaving banks and selecting an alternative lending option. These include hard money, private lenders, and OPM (Other People’s Money or Peer to Peer)). In doing so, they are taking some of the money that was available for new investors and unique investors as well. This in turn causes the pool to shrink even more. What can investors do to stay afloat in these rough waters? They need to be the aggressor and go out looking for lenders that are still able to lend.At Hard Money Mike we always talk about leverage. Real estate is a leverage game and you need to seek out lending opportunities that can provide the leverage you need to win. The reality is that lending opportunities are only going to get worse, It’s not going to get better.

Here’s the upside to that though, the people who learn to play the game with the new lenders are going to have a lot more properties to pick from, and they will have the opportunity to find even better deals than before.You have to be the person out there searching and finding this money so when these deals come, you are going to create wealth.

Here at Hard Money Mike we are still able to lend up to 100% on a really good deal! Watch our most recent video and contact us today to learn more about what we have to offer real estate investors.