DSCR: Will You Be Able to Refinance Your BRRRR Property?

DSCR: Will You Be Able to Refinance Your BRRRR Property?

Today we are going to compare and contrast two properties in order to see how the differences can affect your ability to refinance. Here at Hard Money Mike we do a lot of 100% financing for both the purchase as well as the rehab on a BRRRR property. Before jumping into financing, we also make sure that the property will qualify for a long term loan. One thing that you need to keep in mind is that while you may qualify for a rate and term of 75%, the property may not qualify. Let’s take a look at some numbers to see what that means to you and whether or not you will be able to refinance your BRRRR property.

Look ahead to the refinance before purchasing the property!

More and more people buy a property, get it all fixed up, and then expect to refinance it at 75% to 80%. Unfortunately, when they go to refinance they end up hitting a wall. Oftentimes the property doesn’t qualify for a refinance based on the DSCR ratio. We want to go over a quick example to make sure that you know how to run through the numbers before you purchase that BRRRR.

What do we mean when we say that the property doesn’t qualify?

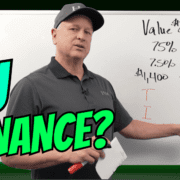

It is important to remember that the numbers have to break even when using the DSCR ratio. This will to keep the interest rates lower. Just to clarify, breaking even means that your rents equal your expenses. While your property and credit score might qualify because they break even, your property might break even at a lower LTV. Why would this occur and why is this different in different zones? Let’s look at the numbers!

Property has a valuation or ARV of $200K

You are looking for a rate and term at 75%

That would be a loan amount of $150K

$200K x .75 = $150K

You get into a BRRRR and you are all in at $150K

Rate of 7.5% would be $1,050 per month for principle and interest on a DSCR loan

What are the rents for this property in different areas?

It is important to research the rents in the area to make sure that your property will break even. One property might rent for $1400 while another would rent for $1800. We want to find the maximum LTV before you purchase a property to see if the property qualifies. While you need to consider your mortgage payment, there are other factors that you need to consider as well. This includes the taxes, insurance, flood insurance (when applicable), and HOA (when applicable). These amounts all have to be added to your payment before comparing it to the rents.

| Property A | Property B | |

| Taxes | $1800 | $3600 |

| Insurance | $1200 | $3600 |

| Flood/HOA | None | $1200 |

| Annual Cost | $3000 | $8400 |

| Monthly Cost | $3000/12 = $250 | $8400/12 = $700 |

| Total Monthly Amount | $1050 + $250 = $1300 | $1050 + $700 = $1750 |

In conclusion,

Before you jump into a BRRRR, or before you find out if you can qualify for 100% financing, make sure that the property qualifies. It is important to find out where your rents are, as well as any additional expenses. These numbers will be helpful to see where the property breaks even. Then you so can make sure you can get the money that you are expecting

If you want to make this easy, reach out to us at Hard Money Mike! We are happy to run through the numbers with you to make sure that you’re able to refinance your BRRRR property.

Watch our most recent video DSCR: Will You Be Able to Refinance Your BRRRR Property?