The Fundamentals of Real Estate Investing: Finding Lenders

Real estate investing is not just about finding great properties. Just as important, you need to find the right funding. In fact, many new investors spend months looking for deals but only a few minutes thinking about lenders. As a result, they often miss opportunities or struggle to close on time.

That is why understanding The Fundamentals of Real Estate Investing: Finding Lenders is so important. The right lender can help you close faster, take on more projects, and grow your business. On the other hand, the wrong lender can create delays, increase costs, and make every deal harder than it needs to be.

Start Looking for Funding Before You Find a Deal

Many new investors make the same mistake. They spend all their time searching for properties and very little time preparing their funding.

Instead, start building your funding team right away. While you learn how to analyze deals and estimate repairs, you should also learn which lenders operate in your market. Furthermore, you should begin building relationships before you ever put a property under contract.

Think about it this way.

Imagine two investors find the exact same deal.

- Investor A already has lenders lined up.

- Investor B starts looking for money after finding the property.

Investor A will usually move faster and have a better chance of closing.

Where to Find Fix and Flip Lenders

Fortunately, there are many lenders that specialize in fix and flip projects. In fact, a large percentage of investor loans come from national lending companies. These lenders often work in multiple states and fund thousands of projects every year.

You can find lenders through:

- Real estate investor groups

- Local meetups

- Online forums

- Investor communities

- Referrals from other investors

- Real estate agents

- Mortgage brokers who work with investors

However, do not stop after finding a lender’s name. Instead, find out which loan officer or originator investors recommend. A great company can have average loan officers, while an average company can have an outstanding one.

What Lenders Look For

Most lenders evaluate two things:

- The deal

- The borrower

Therefore, you need to prepare both.

The Deal

First, lenders want to know if the project makes sense.

They typically review:

- Purchase price

- Repair budget

- After Repair Value (ARV)

- Timeline

- Scope of work

- Exit strategy

For example, a lender feels more comfortable funding a project when an investor clearly explains the budget, repair plan, contractors, and expected timeline. As a result, the lender sees less risk.

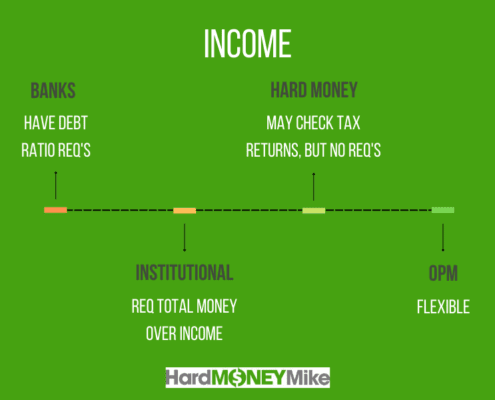

The Borrower

Next, lenders evaluate you.

They often review:

- Credit score

- Experience

- Cash reserves

- Income

- Assets

- Net worth

After all, lenders want confidence that you can finish the project and make payments if challenges arise.

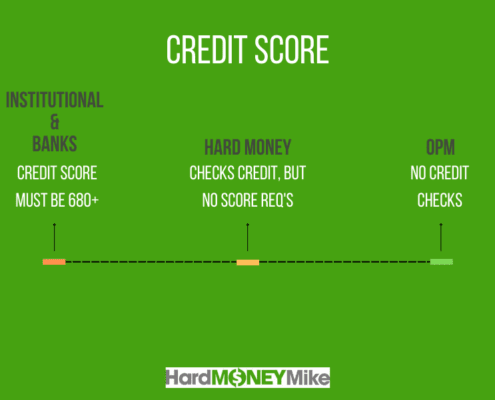

Why Credit Scores Matter

Although fix and flip lenders focus heavily on the property, credit still matters.

Generally speaking:

- 760+ credit scores often receive the best terms.

- 700+ scores typically receive strong financing options.

- 660+ scores can still qualify with many lenders.

- Below 660 may require private money or hard money solutions.

Additionally, higher credit scores often lead to faster approvals and easier underwriting. Therefore, protecting your credit should remain a priority throughout your investing career.

For example, putting large rehab expenses on personal credit cards can hurt your credit utilization ratio. Consequently, your score may drop right before you apply for your next loan.

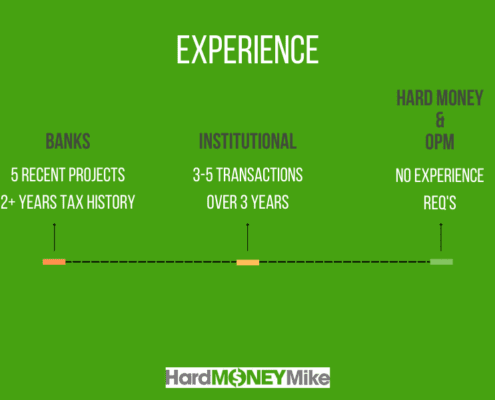

Experience Creates Better Terms

Lenders love experience.

The more projects you complete successfully, the more comfortable lenders become.

As a result, experienced investors often receive:

- Higher leverage

- Better interest rates

- Lower fees

- Faster approvals

However, do not let a lack of experience stop you.

Every successful investor had a first deal.

In the beginning, you may need a larger down payment or more reserves. Yet after a few successful projects, lenders usually become much more flexible.

Cash Reserves Are More Important Than Most Investors Realize

Many new investors believe they only need money for the purchase and repairs.

Unfortunately, that is rarely true.

Lenders want to see reserves because projects almost always have surprises. Furthermore, investors must cover:

- Loan payments

- Utilities

- Insurance

- HOA fees

- Contractor deposits

- Change orders

- Unexpected repairs

Because of this, lenders often review bank accounts, retirement accounts, investment accounts, and business reserves. They want to know you can handle challenges without running out of cash.

A simple rule is this:

The more liquidity you have, the easier the conversation becomes.

Deal Quality Still Rules Everything

Even if you have great credit and plenty of money, lenders still want strong deals.

They look at:

- Loan-to-value ratios

- Repair budgets

- Profit margins

- Timeline

- Backup plans

For instance, lenders often prefer investors who can complete a project in six weeks rather than six months. Shorter projects usually create less risk and better profits.

Additionally, having a backup plan helps.

If your flip does not sell quickly, can it become a rental property?

When lenders see multiple exit strategies, they often feel more confident about the project.

How to Shop for the Right Lender

Many investors focus only on interest rates.

However, that is a mistake.

Instead, evaluate lenders in this order:

1. Can They Fund the Deal?

First and foremost, make sure they can actually close your transaction.

The cheapest lender means nothing if they cannot get the deal approved.

2. Do They Offer Enough Leverage?

Next, determine how much money they will provide.

Some lenders may offer:

- 80% of the purchase price

- 90% of the purchase price

- 100% of the rehab budget

Others may offer less depending on experience and credit. Therefore, find a lender whose leverage matches your needs.

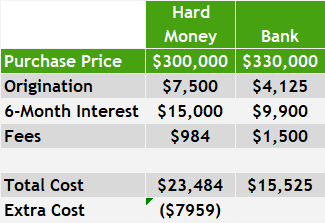

3. What Is the True Cost?

Finally, compare costs.

Look beyond the interest rate.

Review:

- Origination points

- Underwriting fees

- Appraisal fees

- Processing fees

- Exit fees

- Interest rates

For example, one lender may charge higher interest but lower points. Another may charge lower interest but higher points. Depending on your project timeline, either option could be cheaper.

Therefore, always compare the total cost of the loan.

Understand the Draw Process

Many new investors overlook this step.

Most fix and flip lenders do not hand over all rehab money at closing.

Instead, they release funds in stages called draws.

A common example looks like this:

- Complete demolition.

- Request a draw.

- Lender verifies the work.

- Funds are released.

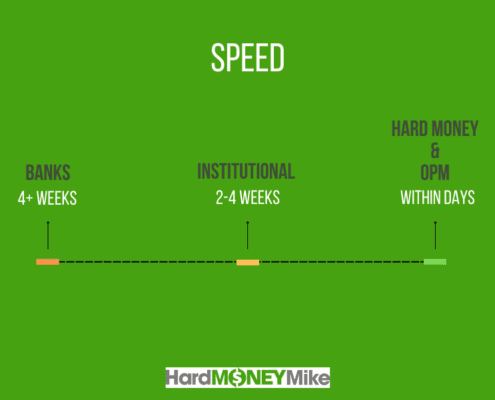

Because of this process, you may need enough cash to pay contractors before reimbursement arrives. Furthermore, some lenders release funds within days, while others take weeks.

As a result, always ask about draw timing before choosing a lender.

Watch for Lender Red Flags

Most lenders are legitimate. Nevertheless, you should stay alert.

Common warning signs include:

- Large upfront fees

- Constant changes to terms

- Poor communication

- Delayed responses

- Unclear pricing

- Refusal to explain costs

Good lenders answer questions. Moreover, they explain their process clearly and communicate throughout the transaction.

If something feels wrong, keep shopping.

There are plenty of lenders available.

Build More Than One Source of Funding

Smart investors rarely rely on a single funding source.

Instead, they build a funding stack.

That stack may include:

- Fix and flip lenders

- Business credit cards

- Lines of credit

- Private lenders

- Equity partners

- Personal reserves

Over time, many investors also develop relationships with private lenders. These relationships often create faster approvals and more flexible terms.

As your business grows, having multiple funding options gives you more flexibility and more opportunities.

The Long-Term Path to Better Financing

The best financing rarely happens on your first deal.

Instead, it happens after you build a track record.

Therefore, focus on:

- Completing projects successfully

- Protecting your credit score

- Building cash reserves

- Growing your experience

- Developing lender relationships

- Creating private funding sources

Over time, lenders compete for experienced investors who perform well. Consequently, financing becomes easier, cheaper, and faster.

Final Thoughts

The Fundamentals of Real Estate Investing: Finding Lenders comes down to one simple idea: prepare your funding before you need it.

First, build relationships with lenders. Next, understand how they evaluate deals. Then, improve your credit, experience, and reserves. Finally, compare leverage, costs, and service before making a decision.

Remember, great investors do not just find good properties. They also build strong funding systems. As a result, they close faster, handle surprises better, and create more opportunities over time. The better you become at finding both deals and funding, the easier real estate investing becomes.

Watch our most recent video to find out more about: The Fundamentals of Real Estate Investing: Finding Lenders